Have you ever felt like no matter how much you try, your money just slips away before the month ends? You pay bills, buy groceries, maybe spend a little on yourself, and suddenly you’re left wondering—where did all my money go? If that sounds familiar, you’re not alone. Many of us struggle to manage income properly, and that’s why tools like the Montly 50 30 20 budget calculator are so useful.

In this blog, we’ll explore how the Montly 50 30 20 budget calculator can make budgeting easier and more stress-free. You’ll learn what

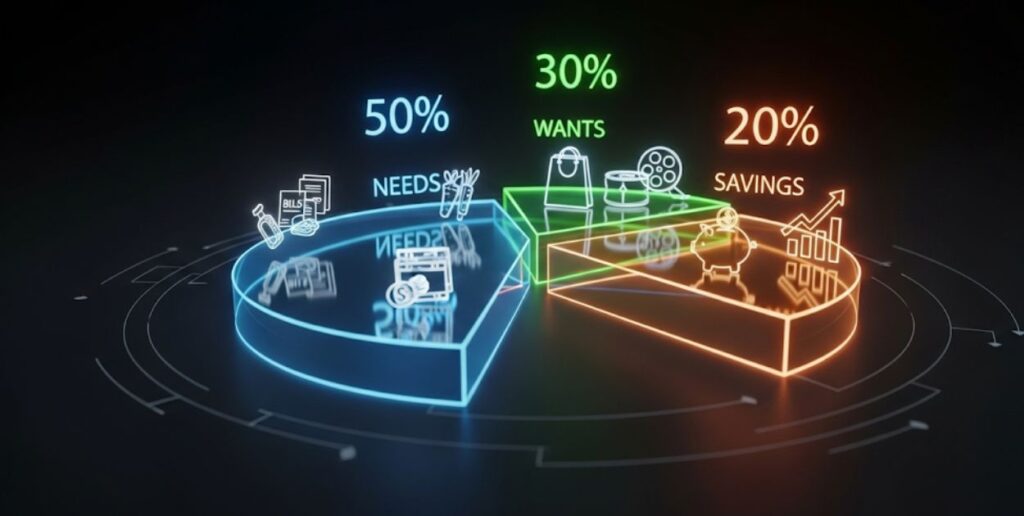

What is the 50/30/20 Rule?

The 50/30/20 rule is one of the most popular personal finance methods in the world. It was first introduced by U.S. Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan. The rule divides your after-tax income into three simple categories:

· 50% for Needs → essentials like rent, utilities, groceries, and healthcare

· 30% for Wants → lifestyle choices like dining out, shopping, hobbies, and entertainment

· 20% for Savings and Debt Repayment → building emergency funds, paying off credit cards, investing for the future

The monthly 50 30 20 budget calculator applies this rule directly to your income, turning abstract percentages into real numbers. Instead of guessing how much you should spend, the calculator gives you a personalized plan.

Why Budgeting Matters in Today’s World

Budgeting is no longer just a suggestion — it’s a necessity. With inflation rising, credit card debt hitting record levels, and the cost of living increasing across the globe, many people find themselves paycheck to paycheck. A budget is like a financial GPS: without it, you’re driving blind.

The monthly 50 30 20 budget calculator helps you:

· Gain control over spending habits

· Avoid unnecessary debt

· Prioritize saving without feeling deprived

· Plan for emergencies and big goals like travel, buying a car, or purchasing a house

Without a clear budget, money often “disappears.” With this calculator, every dollar gets a purpose.

Detailed Explanation of the monthly 50 30 20 budget calculator

50/30/20 Budget Calculator

The calculator takes your monthly after-tax income and splits it according to the 50/30/20 rule. For example:

· If your monthly income is $3,000:

o 50% (Needs) → $1,500

o 30% (Wants) → $900

o 20% (Savings/Debt) → $600

The beauty of the monthly 50 30 20 budget calculator is its flexibility. You can use it for:

· Salaried jobs (fixed income)

· Freelance work (variable income)

· Side hustles and part-time gigs

· Household income (combined earnings of partners)

It adapts to any situation, making it a universal financial planning tool.

How the Formula Works (With Examples)

Let’s break down the monthly 50 30 20 budget calculator with different scenarios:

1. Student Earning $1,200/Month

o Needs (50%) → $600 for rent, food, transport

o Wants (30%) → $360 for fun, Netflix, shopping

o Savings/Debt (20%) → $240 into an emergency fund

2. Young Professional Earning $4,000/Month

o Needs → $2,000 for rent, bills, groceries

o Wants → $1,200 for travel, hobbies, gym

o Savings/Debt → $800 into 401k, debt repayment

3. Family Household Earning $7,500/Month

o Needs → $3,750 for mortgage, utilities, food, car payments

o Wants → $2,250 for vacations, dining out, kids’ activities

Psychology Behind 50/30/20 Budgeting

Money isn’t just math — it’s emotion. Most people overspend because of habits, peer pressure, or instant gratification. The 50/30/20 rule works because it balances both discipline and enjoyment.

· The 50% needs section removes guilt by ensuring essentials are always covered.

· The 30% wants category gives you freedom. You can still enjoy life without overspending.

· The 20% savings ensures you’re building wealth for the future, slowly but steadily.

The monthly 50 30 20 budget calculator brings structure to emotions. It doesn’t tell you to cut out coffee, cancel Netflix, or stop traveling. Instead, it gives you boundaries so you can live your life while preparing for tomorrow.

Deep Dive into the Monthly 50 30 20 Budget Calculator

Understanding the Psychology Behind the 50 30 20 Rule

When people hear about budgeting, they often think it’s about restriction. In reality, the monthly 50 30 20 budget calculator is designed to give you balance. The 50% allocation to needs covers essentials, so you don’t feel deprived of basics. The 30% on wants allows you to enjoy life without guilt, and the 20% on savings and debt repayment builds long-term security.

The psychology here is important: most people overspend because they don’t have a clear framework. The calculator acts as a decision-making guide, preventing emotional overspending and ensuring money aligns with personal goals. By sticking to this structure, you reduce stress about money while still enjoying flexibility.

Detailed Breakdown of Each Category

1. The 50% Needs Category

This category is non-negotiable. The monthly 50 30 20 budget calculator ensures you correctly identify needs versus wants. Needs include housing, utilities, groceries, insurance, transportation, and minimum loan payments.

A common mistake is adding “nice-to-have” expenses into needs. For example, premium cable subscriptions, gym memberships, or dining out don’t truly count as needs. The calculator forces you to separate these items clearly, so your budget is accurate.

Pro Tip: Always list fixed costs first, such as rent or mortgage. Then, add variable essentials like groceries. This way, your “needs” list doesn’t spiral out of control.

2. The 30% Wants Category

This is where most people get confused. Wants include anything that improves lifestyle but is not essential. Examples: streaming subscriptions, vacations, dining out, new clothes, and hobbies.

The monthly 50 30 20 budget calculator is powerful here because it caps lifestyle spending. Without it, many people spend 40–60% of income on wants, leaving little for savings. By limiting to 30%, you still enjoy life but avoid financial regret.

A practical approach is to break this 30% into sub-categories:

· 10% entertainment (movies, Netflix, concerts)

· 10% dining and shopping

· 10% hobbies, travel, or personal upgrades

This breakdown makes the spending plan easier to follow.

3. The 20% Savings and Debt Repayment Category

This section ensures your money builds wealth. The monthly 50 30 20 budget calculator puts emphasis on saving early, even if small.

Breakdown within this 20%:

· Emergency fund: first priority, 3–6 months of expenses

· High-interest debt repayment: second priority

· Investments: retirement accounts, stocks, or mutual funds

· Future goals: down payment for a house, education, or business

Consistency is more important than amount. Even saving 5–10% in the beginning helps build the habit.

Case Studies: Applying the 50 30 20 Calculator in Real Life

Case Study 1: A Young Professional

Sarah earns $3,500 monthly. Using the monthly 50 30 20 budget calculator:

· 50% Needs = $1,750

· 30% Wants = $1,050

· 20% Savings = $700

She realizes her rent and car loan already consume $1,600. After groceries and utilities, her needs hit $1,900, which is over budget. The calculator helps her identify the issue: she either needs cheaper rent or a more affordable car. This awareness allows Sarah to take corrective action.

Case Study 2: A Family with Two Incomes

The Khan family earns $6,000 combined. Their breakdown:

· Needs = $3,000

· Wants = $1,800

· Savings = $1,200

Initially, they were spending $2,500 on wants (vacations, dining, gadgets). The calculator revealed they were overspending by $700 monthly. By adjusting, they redirected $700 into savings, building a fund for their kids’ college.

Case Study 3: A College Student

Ali, a student with part-time income of $1,000:

· Needs = $500

· Wants = $300

· Savings = $200

The monthly 50 30 20 budget calculator showed him that after covering dorm fees and food, he had little left for savings. Instead of ignoring savings, he decided to save just $50 a month. Though small, this habit builds a foundation for financial discipline.

Mistakes to Avoid When Using the Calculator

1. Confusing wants with needs – Luxury items sneak into the needs category.

2. Ignoring irregular expenses – Car repairs, annual subscriptions, and medical bills must be factored in.

3. Not adjusting income changes – If income rises or falls, the calculator must be updated.

4. Forgetting inflation – Costs rise, so needs might increase over time.

5. Neglecting debt repayment – Minimum payments are a need, but aggressive repayment comes from the 20% category.

Avoiding these mistakes ensures accurate and effective budgeting.

Comparing the 50 30 20 Budget Calculator with Other Methods

Envelope System

The envelope method requires cash separation for categories. It’s hands-on but less flexible for digital transactions. The monthly 50 30 20 budget calculator is simpler and modern, better suited for online banking users.

Zero-Based Budget

Zero-based budgeting assigns every single dollar a purpose. It’s detailed but time-consuming. The 50 30 20 method is less strict, giving more freedom while maintaining balance.

70 20 10 Rule

Another budgeting style is 70% needs, 20% savings, 10% wants. This works for those prioritizing savings but sacrifices lifestyle balance. The 50 30 20 rule offers a more enjoyable balance between present and future.

Tools and Apps That Use the 50 30 20 Budget

The monthly 50 30 20 budget calculator can be applied using:

· Mint – Tracks spending and sets categories.

· YNAB (You Need A Budget) – Advanced zero-based budgeting but adaptable to 50 30 20.

· Excel/Google Sheets – Custom calculators for detailed control.

· Banking apps – Many banks offer spending categorization aligned with 50 30 20.

These tools automate tracking, making the process smoother and less stressful.

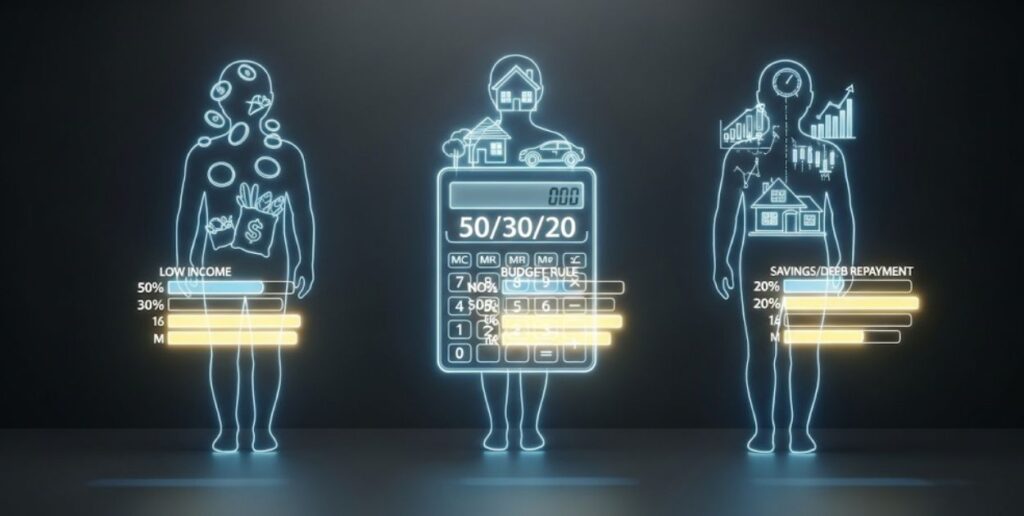

How the Calculator Adapts to Different Incomes

One strength of the monthly 50 30 20 budget calculator is flexibility:

· Low income earners – Focus more on covering needs, even if savings are smaller.

· Middle income earners – Achieve balance between needs, wants, and savings.

· High income earners – May reduce wants to 20% and increase savings to 30–40%.

The framework adjusts to circumstances while maintaining financial discipline.

Long-Term Benefits of Using the Calculator

1. Clarity and control – Know where every dollar goes.

2. Stress reduction – No guessing or worrying about overspending.

3. Debt freedom – Consistent 20% allocation reduces debt quickly.

4. Wealth building – Long-term investments grow with consistency.

5. Lifestyle balance – You enjoy life while securing your future.

This is why financial experts recommend the monthly 50 30 20 budget calculator as a lifelong tool.

Advanced Applications of the Monthly 50 30 20 Budget Calculator

The monthly 50 30 20 budget calculator is more than just a personal finance tool—it’s a flexible system that can be adjusted to meet different lifestyles, financial priorities, and income levels. Once you understand the basics, you can apply this framework in advanced ways to get even more control over your money.

Adjusting the 50 30 20 Budget for Different Income Levels

Not everyone earns the same, and income plays a huge role in how the monthly 50 30 20 budget calculator can be applied.

· Low-income households: For people struggling with necessities, sometimes needs take up 60–70% of income. In this case, the calculator can be adjusted to 60/20/20, where savings are still prioritized, but flexibility is reduced.

· Middle-income earners: Here, the traditional 50/30/20 ratio works perfectly. Needs are manageable, wants are controlled, and savings can grow steadily.

· High-income households: For higher earners, the 50 30 20 calculator can be adapted to 40/20/40. The idea is to use the surplus income to aggressively build investments and long-term wealth.

This adaptability is what makes the method so popular worldwide.

Using the Budget Calculator for Families

Families have unique expenses like childcare, school fees, groceries, and healthcare. The monthly 50 30 20 budget calculator helps families allocate resources fairly.

· 50% Needs: Mortgage/rent, food, medical bills, transportation.

· 30% Wants: Family vacations, dining out, hobbies, Netflix subscriptions.

· 20% Savings: Emergency funds, children’s education savings, retirement funds.

Many families also use joint versions of the calculator so both partners can track shared expenses and stay accountable.

The Role of the Budget Calculator in Debt Management

Debt is one of the biggest obstacles to financial freedom. By applying the monthly 50 30 20 budget calculator, debt repayment can become structured and less overwhelming.

Here’s how:

· Needs (50%) are paid normally, ensuring survival expenses are met.

· Wants (30%) are drastically reduced to speed up debt repayment.

· Savings (20%) can be redirected toward extra loan payments until debt is cleared.

This makes it possible to escape high-interest debt cycles faster.

Monthly 50 30 20 Budget Calculator and Investment Planning

One overlooked advantage of this calculator is its power in investment planning. Once you build an emergency fund, the 20% savings can go into:

· Stocks and bonds

· Mutual funds or ETFs

· Real estate investments

· Retirement accounts (401k, IRA, etc.)

Using this method ensures consistent contributions to your investment portfolio without over-stressing your lifestyle.

How Technology Enhances the Budget Calculator

Today, dozens of mobile apps and online tools integrate the monthly 50 30 20 budget calculator. These digital tools help automate the process.

· Mint: Tracks income and categorizes expenses automatically.

· YNAB (You Need a Budget): Helps with strict allocations.

· Excel/Google Sheets templates: Great for custom calculations.

Technology makes budgeting less of a manual chore and more of a seamless financial habit.

Common Mistakes People Make with the Budget Calculator

Even though the monthly 50 30 20 budget calculator is simple, mistakes are common:

1. Misclassifying wants as needs – For example, dining out isn’t a need, but many treat it as one.

2. Ignoring irregular expenses – Annual insurance premiums or car repairs can throw budgets off.

3. Not adjusting ratios – Sometimes strict 50/30/20 doesn’t fit everyone, but people still force it.

4. Inconsistent tracking – Budgeting works only when updated regularly.

Avoiding these pitfalls ensures long-term success.

Advanced Strategies with the Monthly 50 30 20 Budget Calculator

Now that we’ve explored the fundamentals and benefits of using a monthly 50 30 20 budget calculator, it’s time to dive deeper into more advanced strategies. These techniques can help you optimize your finances, adapt the rule to your personal lifestyle, and unlock long-term wealth creation.

1. Automating Your 50 30 20 Budget

One of the best ways to stick to the 50 30 20 budget is to automate the process. Instead of manually tracking every paycheck, you can:

· Set up automatic transfers: For example, as soon as your salary hits your account, 20% can go straight into savings or investments.

· Use multiple accounts: Have one checking account for needs, another for wants, and a dedicated savings/investment account.

· Leverage digital tools: A monthly 50 30 20 budget calculator integrated with apps like Mint, YNAB, or Personal Capital can help you visualize where your money goes without manual effort.

Automation ensures consistency, reduces human error, and helps you avoid the temptation of overspending.

2. Using the Budget Calculator for Debt Repayment

If you carry credit card balances, student loans, or personal loans, the 20% savings category can be redirected toward debt repayment first. The monthly 50 30 20 budget calculator can help you test different repayment strategies such as:

· Debt Avalanche: Pay off the highest interest rate debt first.

· Debt Snowball: Pay off the smallest debt first to build momentum.

By plugging your numbers into the calculator, you can see how aggressively paying down debt affects your long-term financial health.

3. Adjusting for Lifestyle Changes

Life is dynamic, and your budget should adapt with it. For example:

· Starting a family may increase your needs category (childcare, healthcare).

· Relocating to a cheaper city could lower housing costs, giving you more flexibility in the wants or savings category.

· Career growth or a side hustle could increase your income, allowing you to save more than 20%.

A monthly 50 30 20 budget calculator helps you simulate these scenarios to make smarter choices before the change actually happens.

4. How to Save More Than 20%

While the rule suggests saving 20%, many financial experts argue that aiming for a higher savings rate is key to building wealth. The calculator lets you test variations like 50/20/30 or even 60/20/20, depending on your situation. Strategies include:

· Reducing lifestyle inflation when your income grows.

· Cutting discretionary spending on wants (streaming, subscriptions, luxury items).

· Downsizing housing or transportation to free up more savings.

By adjusting the inputs, you can see exactly how much faster you’ll hit milestones like buying a home or retiring early.

5. Investing with the Help of the Budget Calculator

Savings alone aren’t enough — investing is where wealth grows. You can allocate the 20% savings portion toward:

· Retirement accounts: 401(k), IRA, Roth IRA.

· Brokerage accounts: Stocks, ETFs, index funds.

· Emergency fund: Keeping 3–6 months of expenses in a high-yield savings account.

The monthly 50 30 20 budget calculator helps you balance short-term security with long-term growth by showing how much to direct toward cash savings vs. investments.

6. Tailoring the Rule for Different Income Levels

Not everyone has the same financial flexibility. The calculator makes it easier to adapt the rule for:

· Low-income households: Needs may take up more than 50%. The calculator can help find small savings opportunities without stress.

· Middle-income earners: Ideal for sticking closely to the traditional 50 30 20 split.

· High-income earners: Often can save 30–40% or more by capping lifestyle spending.

This personalization makes the monthly 50 30 20 budget calculator useful for virtually anyone.

7. Tracking Financial Goals with the Calculator

Instead of just budgeting month-to-month, use the calculator to track larger goals:

· Saving for a down payment.

· Building a college fund.

· Planning vacations or weddings.

· Reaching financial independence (FIRE movement).

You can adjust your budget within the calculator to prioritize short-term or long-term goals without losing control over daily expenses.

8. Avoiding Common Mistakes

Many people misuse the 50 30 20 rule. The calculator helps prevent errors such as:

· Misclassifying wants as needs (e.g., dining out isn’t a need).

· Forgetting irregular expenses like car repairs or insurance premiums.

· Saving too little by assuming 20% is enough in all cases.

By running accurate inputs, you avoid underestimating costs and overspending.

FAQs

Q1: What is a monthly 50 30 20 budget calculator?

A monthly 50 30 20 budget calculator helps you divide income into 50% needs, 30% wants, and 20% savings.

Q2: Is the 50 30 20 rule a good way to budget?

Yes, the 50 30 20 rule is a simple and effective way to manage expenses and savings.

Q3: How do I use the monthly 50 30 20 budget calculator?

Just enter your income, and the calculator splits it into needs, wants, and savings automatically.

Q4: Can I use the 50 30 20 budget rule if I earn a low income?

Yes, the 50 30 20 budget rule works for any income, but you may adjust percentages if needed.

Q5: Does the 50 30 20 budget calculator include debt payments?

Yes, debt payments usually fall under the 50% “needs” category in the budget.

Q6: Is the monthly 50 30 20 budget calculator free to use?

Most online monthly 50 30 20 budget calculators are free and easy to access.

Q7: Can I change the percentages in the 50 30 20 rule?

Yes, you can adjust the rule to fit your personal financial goals and lifestyle.

Q8: How does the 50 30 20 rule help with saving money?

It ensures 20% of your income always goes directly into savings or investments.

Q9: Is the 50 30 20 budget calculator better than spreadsheets?

Yes, it’s easier and faster because calculations are done automatically without manual work.

Q10: Who should use the monthly 50 30 20 budget calculator?

Anyone looking to organize their income, control spending, and grow savings can use it.

Welcome To EarnproSavesmarter! I am realAnas an AI Powered SEO , Content Writer With 03 Years Of Experience.I Help Website Rank Higher, Grow Traffic ,And Look Amazing. My Goal is To Make SEO And Content Writing Simple And Effective For Everyone.

Let’s Achieve More Together.