Choosing health insurance in the U.S. can feel overwhelming. You scroll through endless options, compare confusing premiums, and wonder if you’re making the right choice—or just paying too much. It’s easy to feel frustrated or unsure, especially when your health and finances are on the line.

In this guide, we’ll break down the best health insurance plans in the US and help you understand your options. From employer-sponsored coverage to affordable marketplace plans, state-specific insights, and real-life tips, you’ll get clear, practical advice to pick the plan that fits your needs without the guesswork.

Types of Health Insurance Plans in the US

Before diving into which insurer ranks at the top, it’s important to understand the main types of health insurance. Each plan type comes with unique rules, networks, and costs. Picking the wrong one could mean paying more or struggling to see your preferred doctor.

Health Maintenance Organization (HMO)

HMOs are known for being cost-effective. You pick a primary care doctor, get referrals for specialists, and stick to a network. They’re ideal if you want lower premiums and don’t mind limited flexibility. For example, if you need a dermatologist, you must first see your family doctor before getting a referral. The catch? Step outside the network, and you’re often on the hook for the full bill.

Preferred Provider Organization (PPO)

If freedom is your priority, PPOs shine. You don’t need referrals, and you can see out-of-network doctors—though at a higher cost. Many Reddit users describe PPOs as “the least terrible” option, especially if they want access to specific prescriptions or specialists. However, PPOs typically come with higher premiums, making them best suited for those who value choice over savings.

Exclusive Provider Organization (EPO)

EPOs sit between HMOs and PPOs. You don’t need referrals, but you must stay within the network to be covered. They usually cost less than PPOs but more than HMOs. For many families, EPOs strike the right balance between affordability and flexibility.

Point-of-Service Plan (POS)

POS plans combine features of HMOs and PPOs. You need referrals for specialists, but you can sometimes get partial coverage out of network. They’re less common but worth exploring if your employer offers them.

High-Deductible Plans & HSAs

Some people prefer high-deductible health plans (HDHPs) paired with a Health Savings Account (HSA). With these, you pay lower monthly premiums but take on more upfront costs until you reach your deductible. The upside is that HSA contributions are tax-free, and your employer might add funds too. If you’re young, healthy, and rarely visit the doctor, this setup can save you money.

Top Health Insurance Companies in the US

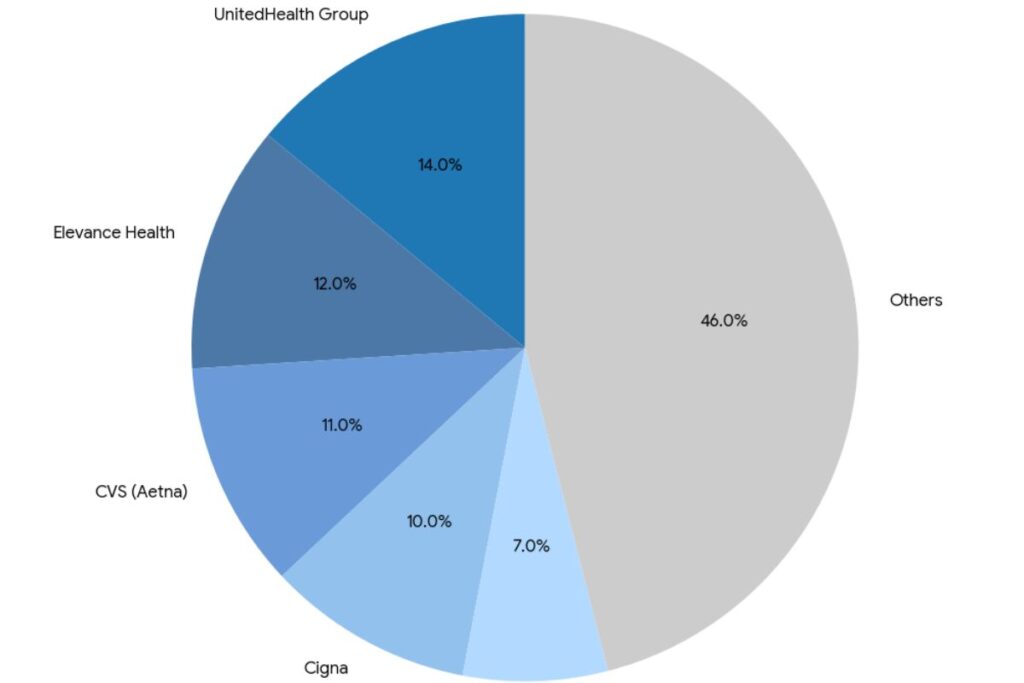

Not all insurers are created equal. Some dominate the market with billions in premiums, while others serve specific regions. Here’s a breakdown of the biggest players, based on the NAIC Health Insurance Report 2023.

UnitedHealth Group

As the market leader, UnitedHealth pulled in over $248 billion in premiums in 2023. With a vast network and strong PPO options, it’s a top pick for large employers and individuals who want broad coverage. Many users praise its flexibility, though some complain about complex claim processes.

Elevance Health (Anthem)

Formerly known as Anthem, Elevance is a powerhouse in many states, particularly with Blue Cross Blue Shield (BCBS) plans. It’s often the go-to for employer-sponsored coverage and offers competitive HMO and PPO options.

CVS Health / Aetna

After CVS acquired Aetna, the insurer expanded its reach with integrated pharmacy and health services. For people who want strong prescription coverage, especially with chronic conditions, Aetna often ranks high.

Kaiser Foundation (Kaiser Permanente)

Kaiser is unique because it’s both an insurance company and a healthcare provider. This integrated model means care and insurance are under one roof. Supporters love the streamlined experience, but critics say it creates a conflict of interest—Kaiser decides both what’s covered and how care is delivered.

Cigna Health

Cigna has a large national network and is well-regarded for its international coverage. Expats and frequent travelers often choose it.

Humana

Known for Medicare Advantage plans, Humana is a strong option for seniors. If you’re nearing retirement, this is a company worth exploring.

Centene Corp.

Centene specializes in Medicaid and ACA marketplace plans, making it vital for lower-income individuals and families.

Blue Cross Blue Shield (State Plans)

BCBS isn’t a single company but a federation of state-based insurers. Plans like Florida Blue (GuideWell), Blue Cross NC, and BCBS Massachusetts dominate their local markets. In fact, many state residents think of BCBS as “the default” health insurance.

Other Notable Insurers

- Molina Healthcare – Strong in Medicaid and low-cost plans.

- HCSC (Health Care Service Corporation) – Operates BCBS in five states.

- Independence Health Group – Big player in Pennsylvania.

- Highmark Group – Prominent in the Northeast.

- Carefirst Inc. – Strong in Maryland/DC.

- UPMC Health System – Based in Pennsylvania, integrated with hospitals.

- Point32Health – Focused on Massachusetts.

- CareSource, Health Net, Local Initiative Health Authority – Regional players serving Medicaid and marketplace enrollees.

Best Health Insurance Plans by state

One of the most confusing parts of US healthcare is that your options vary by state. For instance, Kaiser dominates California, while GuideWell (Florida Blue) is strong in Florida. In New York, EmblemHealth and Empire BCBS are major players.

Case Studies by State

To enrich your article, we’ll create state clusters with 4–5 examples each. Each case study will highlight:

- Most popular insurer in that state

- Why locals prefer it

- Average costs (family vs. individual premiums)

- Reddit/real-life insight

Example (draft style):

California

California is home to Kaiser Permanente, which dominates the state with its integrated HMO model. Many families choose Kaiser because of the convenience of having insurance and care under one roof. However, Reddit threads often highlight frustrations with wait times. For those who want flexibility, Blue Shield of California offers PPO options.

- Average Family Premium (2024): $25,900

- Average Self-Only Premium: $9,100

- Best For: Families who want affordable, predictable care

Florida

In Florida, GuideWell (Florida Blue) is the most recognized name. It’s the top choice for both ACA marketplace enrollees and employer-sponsored coverage. Many small business owners in Florida report that the SHOP marketplace combined with BCBS plans makes offering health benefits financially feasible.

- Average Family Premium (2024): $25,300

- Average Self-Only Premium: $8,900

- Best For: Small businesses, middle-income families

Texas

Texas leans heavily on HCSC (Blue Cross Blue Shield of Texas). Reddit users often note it’s “the default” option through employers. For individuals, Centene and Molina Healthcare provide some of the cheapest ACA marketplace plans.

- Average Family Premium (2024): $25,500

- Best For: Employer-sponsored coverage, Medicaid expansion plans

How to Choose the Best Health Insurance Plan

Choosing a health insurance plan in the U.S. often feels like solving a puzzle. You’re balancing monthly premiums, out-of-pocket costs, and which doctors are included. Many people focus only on the lowest monthly premium, but that can backfire if the plan has a small provider network or high deductibles.

A smart way to compare plans is by looking at the “total annual cost” — not just the premium. That means adding your expected out-of-pocket healthcare expenses to the yearly premiums. For example, a Reddit user once shared how their cheap ACA bronze plan ended up costing more than a silver plan because of high deductibles after one hospital visit.

Key Factors to Consider

When reviewing options, here are the factors that matter most:

- Network Type (HMO, PPO, EPO, POS):

- HMO plans usually cost less but lock you into a specific network.

- PPO plans offer freedom to see specialists without referrals, though premiums are higher.

- EPOs are a hybrid with limited out-of-network coverage.

- POS plans require referrals but sometimes allow partial out-of-network care.

- Premiums vs. Deductibles: Don’t get trapped by a low premium with sky-high deductibles. A balance often works better for families.

- Out-of-Pocket Maximums: This number caps what you’ll ever pay in a year. If you have chronic health issues, this matters more than monthly premium cost.

- Employer-Sponsored vs. Individual: Employer plans often subsidize a large portion (average $19,276 for family coverage in 2024), while individual ACA marketplace plans may suit freelancers.

- Health Reimbursement Options (HRAs): Employers increasingly offer ICHRA and QSEHRA to reimburse employees tax-free, letting workers pick their own plans while still receiving support.

- State-Specific Benefits: Some states expand ACA coverage further than others. For example, New York and California often have stronger marketplace subsidies compared to Texas.

Health Insurance Plan Decision Flowchart

Answer the questions below to find the best health insurance option for you.

Do you get insurance from your employer?

Compare employer plan vs HRA options (ICHRA, QSEHRA, GCHRA). Minimum participation: 70%

Do you want maximum flexibility or lower cost?

Go to ACA Marketplace. Do you qualify for Medicaid/CHIP?

Medicaid/CHIP (free or low-cost coverage)

Compare ACA Metal Tiers: Bronze, Silver, Gold

Bronze Plan: Lowest premiums, high deductibles. Best for young/healthy individuals who want basic coverage.

Silver/Gold Plan: Moderate to higher premiums, lower out-of-pocket costs. Best for families or people with frequent medical needs.

Best Cheap Health Insurance Plans in the USA

Finding affordable coverage isn’t easy. Many families worry about paying high monthly premiums, while others stress about out-of-pocket costs when visiting a doctor. The truth is, the best health insurance plans in the US for budget-conscious people often come through the ACA Marketplace or Medicaid, depending on your income. For example, in 2024, the average self-only premium was $8,951, while family coverage reached $25,572. Employers usually pay part of this bill, but if you’re on your own, the sticker shock can be overwhelming.

That’s where cheaper options step in. Bronze-tier ACA plans usually have the lowest monthly cost, though you’ll pay more if you need care. They’re a good fit for young, healthy individuals who don’t visit the doctor often. Silver plans, on the other hand, balance affordability with decent coverage, especially if you qualify for subsidies. Families with children sometimes find that Medicaid or CHIP offers nearly free healthcare if their income falls under state guidelines. A Reddit user summed it up perfectly: “If you reframe your thinking to which is the least terrible, you’ll be in a better position to accept your findings.” In other words, the “best” cheap plan is often the one that hurts your wallet the least while still covering emergencies.

Employer coverage can also be surprisingly affordable. If your workplace offers group health insurance plans, you might pay far less compared to buying directly from an insurer. One employee shared how his company’s PPO plan covered both his regular doctors and expensive prescriptions with a small copay. This shows why exploring every option—employer plans, ACA Marketplace, or Medicaid—is critical before deciding what’s truly “cheap” for you.

Comparison of Affordable ACA Health Insurance Plans

| Plan Type | Monthly Premium | Deductible | Best For | Pros | Cons |

| Bronze Plan | Lowest | Highest | Young, healthy individuals | Low monthly cost; covers essential health benefits | High out-of-pocket costs when you need care |

| Silver Plan | Moderate | Moderate | Families, middle-income earners | Balance of premium vs. coverage; cost-sharing reductions if you qualify | Higher monthly payment than Bronze |

| Gold Plan | Higher | Low to moderate | People with frequent medical needs | Low out-of-pocket expenses; predictable healthcare costs | Expensive premiums; may not be cost-effective if you’re healthy |

💡 Many people think of Bronze plans as a safety net—cheap each month, but risky if you get sick. Silver often turns out to be the best health insurance plan in the US for those who qualify for subsidies. Gold shines for people managing chronic conditions, since frequent doctor visits quickly offset higher premiums.

Real-Life Case Studies: Choosing the Best Health Insurance Plan in the US

Case Study 1: Sarah the Freelancer (Bronze Plan)

Sarah, a 27-year-old graphic designer, works independently and pays for her own insurance. She’s healthy, rarely visits the doctor, and prefers to save money each month. A Bronze plan gives her the lowest premium, covering emergencies while keeping costs down. She knows if she ever faces a major accident, the plan will protect her from devastating medical bills.

Case Study 2: David the Small Business Owner (Silver Plan with HRA)

David runs a 10-person marketing agency. Instead of offering a traditional group health insurance plan, he uses an Individual Coverage HRA (ICHRA). His employees choose their own Silver plans on the ACA marketplace, while David reimburses them tax-free. This way, his business controls costs, and employees enjoy personalized coverage. It’s a win-win for flexibility and affordability.

Case Study 3: The Johnson Family of Four (Silver Plan with Subsidy)

The Johnsons, a middle-income family in Ohio, qualify for cost-sharing reductions under the Affordable Care Act. By choosing a Silver plan, their monthly premiums stay affordable, and their out-of-pocket expenses are much lower. With two kids who need regular checkups and prescriptions, the Silver plan strikes the right balance between cost and coverage.

Case Study 4: Linda the Early Retiree (Gold Plan)

At 61, Linda retired early but isn’t eligible for Medicare yet. She has diabetes and visits specialists frequently. A Gold plan works best for her because it keeps deductibles low and reduces surprise medical bills. While her premiums are higher, predictable costs give her peace of mind during retirement.

👉 These examples highlight why there’s no single “perfect” option. The best health insurance plans in the US depend on lifestyle, income, and medical needs.

How to Choose the Best Health Insurance Plan

When it comes to picking a health insurance plan, there isn’t a one-size-fits-all answer. The right plan depends on your lifestyle, health needs, and budget. Start by looking at the monthly premiums, deductibles, and out-of-pocket costs. A lower monthly premium often means higher out-of-pocket expenses when you need care, while higher premiums usually give you more predictable costs.

Another critical step is checking the provider network. If you already have doctors you trust, make sure they’re in the plan’s network. Out-of-network care can be extremely expensive, especially with HMOs and EPOs that don’t cover those costs. Consider whether you’ll need frequent specialist visits, prescription medications, or mental health services, as these benefits vary widely between plans.

Factors to Consider Before Enrolling

- Coverage needs: Do you need family coverage, maternity care, or specialized treatment?

- Budget: Balance between premium, deductible, and coinsurance.

- Flexibility: PPOs give more freedom but cost more, while HMOs are cheaper but more restrictive.

- Employer support: If offered, employer-sponsored coverage is often more affordable due to contributions.

- ACA compliance: Marketplace plans guarantee essential benefits like preventive care, ER visits, and prescription drugs.

Flowchart: Quick Decision Guide

I can create a simple decision-making flowchart (like: “Do you want lowest monthly cost? →

Best Health Insurance Plans by State

This section will break down how the best health insurance plans in the US vary depending on location. Every state has its own marketplace rules, top providers, and affordability trends. I’ll expand this with state-level highlights, mini case studies, and even add a regional comparison table for clarity.

Best Health Insurance Plans by State

California

Common leaders: Kaiser Permanente (HMO), Blue Shield of California, Anthem Blue Cross, Health Net.

What often works: HMOs dominate for affordability; PPO/EPO via Blue Shield or Anthem for flexibility.

Mini story: Maya lives in San Diego and wants predictable costs for her toddler’s visits. She picks a Kaiser HMO for low copays and same-system specialists. Her partner, who travels for work, chooses a Blue Shield PPO to keep out-of-network options open.

Texas

Common leaders: Blue Cross and Blue Shield of Texas (HCSC), UnitedHealthcare, Aetna, Molina, Ambetter (Centene).

What often works: PPOs via BCBS for employer groups; marketplace shoppers compare Ambetter/Molina for lower premiums vs. BCBS PPO for broader networks.

Mini story: Javi runs a small HVAC business in Austin. Instead of one group plan, he sets up an ICHRA so each employee picks a Silver marketplace plan and gets tax-free reimbursement.

Florida

Common leaders: Florida Blue (GuideWell), UnitedHealthcare, Aetna, Ambetter (Centene), Molina.

What often works: Florida Blue for broad networks; Ambetter/Molina for lower marketplace premiums; HMOs/EPOs are common.

Mini story: The Rodriguezes qualify for cost-sharing reductions. A Silver Florida Blue HMO cuts their specialist copays in half compared with Bronze.

New York

Common leaders: Empire BlueCross BlueShield, Fidelis Care, EmblemHealth, UnitedHealthcare, MVP.

What often works: Strong marketplace options; check networks carefully—downstate vs upstate varies.

Mini story: Priya in Queens needs her OB/GYN. She sorts plans by “doctor in network” first, then picks an Empire EPO that keeps premiums reasonable without referral hassles.

Pennsylvania

Common leaders: Highmark BCBS, Independence Blue Cross, UPMC Health Plan, Aetna, UnitedHealthcare.

What often works: Regional strength matters—UPMC vs. Highmark varies by county; employer PPOs are popular.

Mini story: Dan in Pittsburgh has a UPMC cardiologist he loves. He pays a bit more for a UPMC Gold plan so his max out-of-pocket is lower for specialist care.

Illinois

Common leaders: Blue Cross and Blue Shield of Illinois (HCSC), Aetna, UnitedHealthcare, Ambetter, Cigna.

What often works: BCBSIL PPOs for large networks; Ambetter for budget shoppers in metro areas.

Mini story: A Chicago freelancer switches from a Bronze PPO to a Silver plan after a single ER bill shows how quickly deductibles matter.

Ohio

Common leaders: Anthem (Elevance), Medical Mutual, Molina, CareSource, Aetna.

What often works: Silver marketplace plans with CSR for families; Medical Mutual PPOs for broad access.

Mini story: The Johnsons (family of four) choose a Silver CSR plan so their kid’s asthma meds and specialist visits don’t blow the budget.

Georgia

Common leaders: Anthem (Blue Cross Blue Shield of Georgia), Ambetter (Peach State), Kaiser, Aetna, Cigna.

What often works: Ambetter for aggressive marketplace pricing; Kaiser HMO where available; BCBS GA for employer PPOs.

Mini story: Tiana near Atlanta wants mental-health coverage. She picks a plan with transparent therapist copays—even if the premium’s a touch higher.

North Carolina

Common leaders: Blue Cross and Blue Shield of North Carolina, UnitedHealthcare, Aetna, Cigna.

What often works: BCBSNC has wide reach; compare EPO vs PPO by county; Medicaid expansion impacts eligibility.

Mini story: A newly self-employed couple in Raleigh uses an HSA-eligible Bronze plan to lower premiums, then funds the HSA with part of their tax refund.

Michigan

Common leaders: Blue Cross Blue Shield of Michigan, Priority Health, Molina, Meridian (Centene).

What often works: Priority Health for strong managed-care networks; BCBSM for broad acceptance.

Mini story: A Grand Rapids teacher picks Priority Health HMO through her district for predictable copays and good maternity coverage.

New Jersey

Common leaders: Horizon Blue Cross Blue Shield of NJ, AmeriHealth, Aetna, Oscar (select areas).

What often works: Horizon for statewide depth; Oscar’s EPOs in urban counties appeal to digital-first users.

Mini story: Sal in Jersey City wants virtual care on evenings. He picks Oscar for app-based visits and easy e-prescriptions.

Arizona

Common leaders: Blue Cross Blue Shield of Arizona, Ambetter, UnitedHealthcare, Aetna, Cigna.

What often works: Marketplace shoppers compare Ambetter vs BCBSAZ; snowbirds should verify national networks.

Mini story: A seasonal resident keeps a PPO so winter specialists in Phoenix and summer providers out of state both stay in reach.

Washington

Common leaders: Premera Blue Cross, Regence BlueShield, Kaiser Permanente WA, Molina.

What often works: Kaiser integrated care in Puget Sound; Premera/Regence PPOs for broader networks statewide.

Mini story: An engineer in Redmond picks a Kaiser Silver for price and convenience; her partner chooses a Premera PPO for out-of-network freedom.

Massachusetts

Common leaders: Blue Cross Blue Shield of Massachusetts, Tufts Health Plan (Point32Health), Harvard Pilgrim (Point32Health).

What often works: Strong HMO/EPO offerings; employer plans are often rich in benefits.

Mini story: A biotech analyst in Cambridge chooses BCBSMA Gold—higher premium, but predictable specialist costs during a demanding year.

Virginia

Employer-Sponsored & Small Business Health Insurance

Employer-sponsored coverage is often the most cost-effective way to get health insurance in the US. Many companies contribute significantly to premiums, lowering your monthly out-of-pocket costs. For families and individuals, this can make a huge difference compared to buying coverage independently through the ACA marketplace.

Most group health insurance plans require a minimum participation rate—typically around 70% of eligible employees—to maintain affordability and meet underwriting requirements. If your company qualifies, options like QSEHRA (Qualified Small Employer HRA), ICHRA (Individual Coverage HRA), and GCHRA (General HRA) allow employers to provide tax-free reimbursements for employees who select their own insurance plans. These arrangements give workers flexibility while keeping company costs predictable.

Companies like PeopleKeep and Remodel Health have made it easier for small businesses to manage these HRAs. By integrating administration software, they streamline reimbursements, track participation, and ensure compliance. This combination of flexibility, tax benefits, and ease of use has made employer-sponsored coverage a strong contender for small businesses aiming to offer competitive health benefits without breaking the budget.

Alternative Coverage Options

Not every employee or individual fits neatly into traditional insurance plans. Health Reimbursement Arrangements (HRAs) provide a flexible alternative by reimbursing medical expenses or insurance premiums tax-free. Unlike traditional group plans, HRAs allow employees to select coverage that matches their specific health needs, which is particularly attractive for freelancers and part-time workers.

Some employers also offer health stipends, which are flat-dollar allowances to cover medical costs. This approach gives workers freedom while controlling company spending.

For young, generally healthy individuals, catastrophic plans are another affordable option. These plans have low monthly premiums but high deductibles and are primarily designed to protect against major medical events. Reddit users often note that catastrophic plans are “perfect for emergencies without breaking the bank month-to-month,” making them a viable choice for students, early-career professionals, or anyone on a tight budget.

Cost of Health Insurance in the US

Health insurance costs in the US vary widely depending on plan type, employer contributions, and state-specific subsidies. According to KFF 2024 data, the average self-only premium is $8,951, while family coverage averages $25,572. Employers typically contribute $7,584 for single coverage and $19,276 for family plans, which significantly offsets individual expenses.

Here’s a breakdown of typical costs:

- Deductibles: $1,500–$7,000 (varies by plan tier)

- Co-pays: $15–$50 for doctor visits, $30–$100 for specialists

- Coinsurance: 10–30% after deductible, depending on plan

- Out-of-pocket maximum: $6,000–$15,000 for individuals; $12,000–$30,000 for families

Understanding the total annual cost—not just the monthly premium—is essential to avoid surprises. Many Reddit users have shared stories where low premiums seemed attractive until a single ER visit or surgery revealed the true cost of high deductibles and coinsurance.

Trends in Health Insurance 2025

The health insurance landscape is evolving rapidly. Technology is playing a larger role, with administration software and AI claims processing streamlining plan management and customer service. Employers are increasingly adopting HRAs and health stipends, offering flexible, tax-advantaged alternatives to traditional plans.

Self-insurance is also on the rise. Big companies like Google and Apple are moving away from fully insured plans, choosing to cover their employees directly while using third-party administrators. Meanwhile, consumers are demanding more comprehensive coverage, including mental health services and prescription drug benefits, reflecting a growing emphasis on holistic wellness rather than reactive care.

FAQs

What is the best health insurance in the US?

The best insurance depends on your needs, budget, and location. Employer plans, ACA marketplace coverage, and Medicaid all serve different purposes.

Which is the best health insurance plan?

There’s no single answer—it varies based on family size, health needs, and whether you prioritize low premiums or network flexibility.

How much does 100% health insurance cost in the USA?

For comprehensive employer-sponsored plans, employers often cover most costs. Individual plans range widely; self-only coverage averages $8,951/year, and family plans around $25,572/year.

Who are the top 5 insurance companies in the US?

UnitedHealth Group, Elevance Health (Anthem), CVS Health/Aetna, Kaiser Permanente, and Humana dominate the market.

Which private health insurance is best?

It depends on your needs. PPOs are best for flexibility; HMOs for affordability; Gold plans for frequent care; Bronze for low-cost emergency coverage.

What’s the best medical insurance Reddit recommends?

Reddit users favor plans that balance premiums with out-of-pocket costs and network access. Silver-tier ACA plans often receive praise for cost-sharing reductions and reasonable deductibles.

Conclusion

There’s no one-size-fits-all solution when it comes to health insurance in the US. The best health insurance plans in the US depend on your location, health needs, budget, and whether your employer offers coverage. Always compare plans annually, considering premiums, deductibles, network access, and any available subsidies. By staying informed and reviewing options each year, you can ensure the coverage you choose protects both your health and your finances.

Welcome To EarnproSavesmarter! I am realAnas an AI Powered SEO , Content Writer With 03 Years Of Experience.I Help Website Rank Higher, Grow Traffic ,And Look Amazing. My Goal is To Make SEO And Content Writing Simple And Effective For Everyone.

Let’s Achieve More Together.