Sometimes saving for retirement feels confusing—you know it’s important, but the terms, options, and rules make it overwhelming. You may even wonder if your money will really grow enough to support you later in life. That’s where understanding a 401(k plan can make all the difference.

In this blog, we’ll break down everything you need to know about a 401(k plan in simple, clear language. From how it works and the benefits it offers, to smart strategies for growing your savings, you’ll get the answers you’ve been searching for.

What Is a 401(k) Plan and How Does It Work?

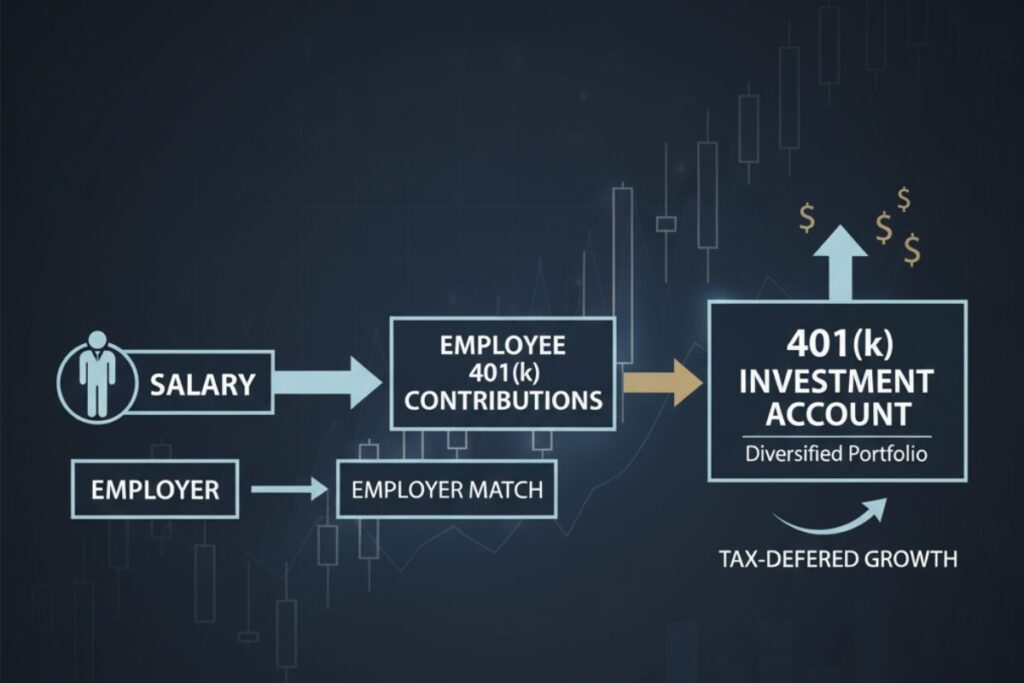

A 401(k) plan is a retirement savings account offered by many employers in the United States. When you sign up, a portion of your paycheck is automatically set aside and invested into the account. The biggest advantage is that you don’t need to think about saving each month—the money is deducted before you even see it. Over time, these contributions grow thanks to compound interest and investment returns.

The plan gets its name from a section of the IRS tax code. What makes it unique is the way taxes are handled. With a traditional 401(k), your contributions are made before taxes are taken out, which lowers your taxable income for the year. The money grows tax-deferred, meaning you don’t pay taxes on it until you withdraw in retirement. This simple structure helps millions of people build steady retirement savings while reducing their yearly tax burden.

Types of 401(k) Plans You Should Know

Not every 401(k) plan looks the same. Depending on your job and financial goals, you might have access to different types of retirement accounts. Understanding the options helps you make smarter choices about your retirement savings.

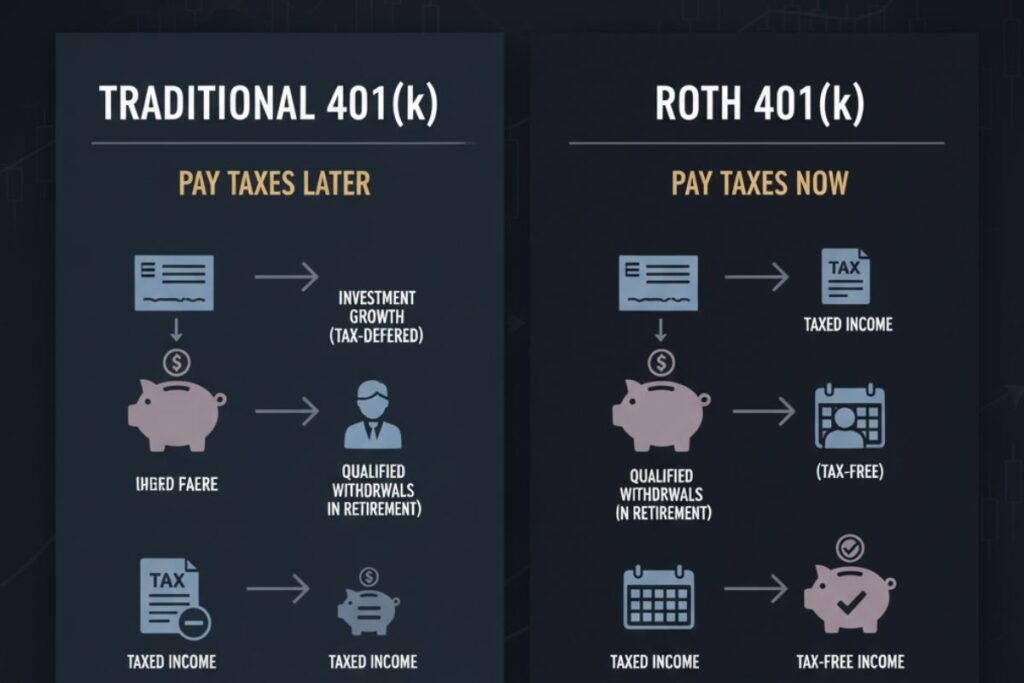

Traditional 401(k)

The traditional 401(k) is the most common version. Your contributions are made with pre-tax dollars, which means you pay less in income taxes now. The money then grows tax-deferred, and you’ll pay taxes when you withdraw during retirement. For many workers, this setup offers immediate tax benefits while they’re in higher-earning years.

Roth 401(k)

A Roth 401(k) works the opposite way. You contribute after-tax dollars, so there’s no upfront tax break. However, the withdrawals in retirement are tax-free, including all investment growth. This makes it an attractive choice if you expect to be in a higher tax bracket later in life. Think of it as paying the tax bill today so your future retirement income is worry-free.

Solo 401(k)

If you’re self-employed or running a small business without employees, the solo 401(k) is designed for you. It lets you save as both an employee and an employer, meaning much higher contribution limits. This option is especially powerful for freelancers, consultants, and entrepreneurs who want more control over their retirement account.

Key Benefits of a 401(k) Plan

The real strength of a 401(k) plan lies in the benefits it offers compared to other retirement savings options. It’s not just about putting money aside—it’s about how that money grows and multiplies over time.

One of the biggest advantages is the employer match. Many companies will contribute extra money to your account based on how much you save. For example, if your employer matches 50% of contributions up to 6% of your salary and you earn $60,000 a year, contributing $3,600 gets you an additional $1,800 for free. That’s essentially extra retirement income without any effort on your part.

Another major benefit is the tax advantage. With a traditional 401(k), you get an immediate tax break since contributions reduce your taxable income. With a Roth 401(k), the tax benefit comes later, because your withdrawals during retirement are completely tax-free. Either way, these tax benefits help your money grow faster and keep more of your hard-earned savings in your retirement account.

Over time, the combination of compound growth, employer contributions, and tax savings can turn even small monthly contributions into a significant nest egg for your financial future.

Contribution Limits and IRS Rules

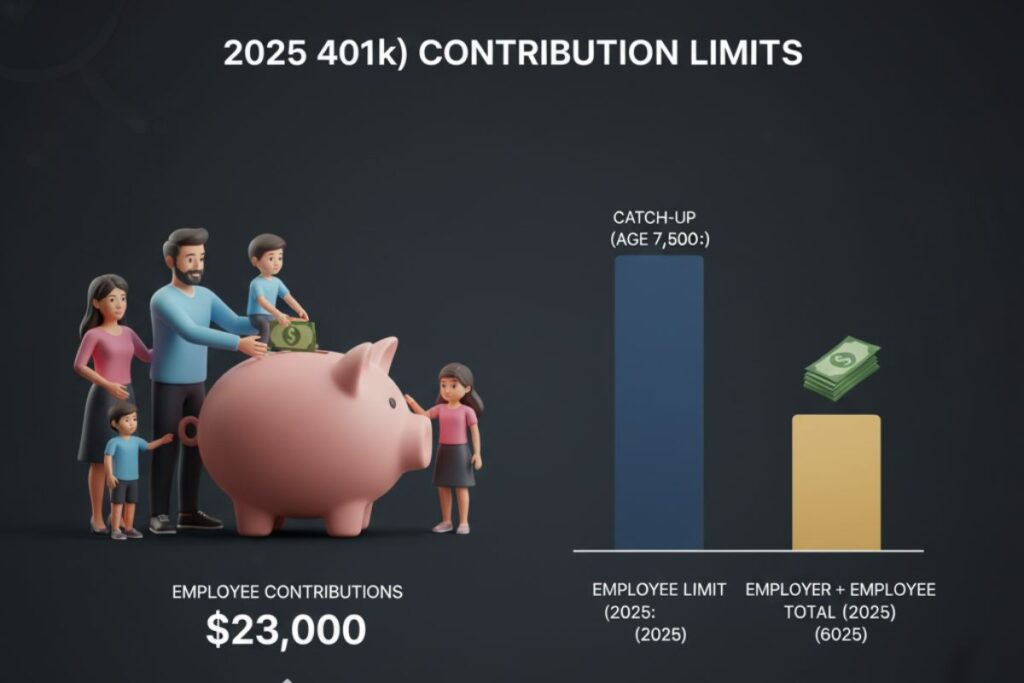

Every 401(k) plan comes with rules set by the IRS to keep retirement savings fair and consistent. One of the most important rules is the contribution limit—the maximum amount you’re allowed to put into your retirement account each year. These limits are updated regularly to keep up with inflation and changing economic conditions.

For 2025, the annual employee contribution limit is $23,000. If you’re age 50 or older, you can make an additional catch-up contribution of $7,500, bringing your total to $30,500. These extra contributions are designed to help older workers boost their retirement savings as they get closer to retirement age.

It’s also worth noting that there’s a combined limit when you factor in both employee and employer contributions. Together, the total cannot exceed $69,000 for workers under 50, or $76,500 for those using the catch-up provision. Staying within these IRS limits ensures that your 401(k) plan keeps its tax benefits and remains in good standing.

Vesting and Employer Matching Explained

One of the unique features of a 401(k) plan is the employer match, but how much of that money you actually keep depends on something called vesting. Vesting refers to how much of your employer’s contributions you own if you leave the company. While your personal contributions always belong to you, the employer match often follows a schedule.

For example, some companies offer immediate vesting, which means you get 100% of the employer match right away. Others use a gradual vesting schedule where you earn ownership over time—say 20% after the first year, 40% after the second, and so on until you’re fully vested after five years. If you leave before you’re fully vested, you might lose part of the employer’s contributions.

This makes it important to understand your company’s rules. Staying at a job just a little longer could mean thousands of extra dollars in your retirement account, directly boosting your long-term savings.

Investment Options Inside a 401(k)

A 401(k) plan isn’t just about saving—it’s also about investing. When you put money into your retirement account, it doesn’t just sit there; it’s invested in a variety of options that can help your savings grow over time. The choices available depend on your employer’s plan, but most include a mix of stocks, bonds, mutual funds, and exchange-traded funds (ETFs).

Diversification is the key to managing risk. Stocks may offer higher growth potential, but they’re also more volatile. Bonds provide more stability, while mutual funds and ETFs offer a balanced approach. Many plans also include target-date funds, which automatically adjust your mix of investments as you get closer to retirement.

Here’s a simple breakdown of common investment options:

| Investment Option | Risk Level | Growth Potential | Best For |

| Stocks | High | High | Long-term growth |

| Bonds | Low | Moderate | Stability & income |

| Mutual Funds | Medium | Moderate to High | Diversification |

| ETFs | Medium | Moderate to High | Flexibility & low cost |

| Target-Date Funds | Varies | Balanced | Hands-off investors |

Choosing the right mix depends on your risk tolerance, financial goals, and how far you are from retirement. A younger worker might lean more toward stocks, while someone nearing retirement may prefer safer options like bonds.

Withdrawal Rules and Penalties

A 401(k) plan is meant to be a long-term retirement savings tool, which is why the IRS has strict withdrawal rules. In most cases, you can’t take money out without penalties until you reach age 59½. If you withdraw earlier, you’ll usually face a 10% early withdrawal penalty on top of regular income taxes.

There are some exceptions, like hardship withdrawals for major expenses such as medical bills or buying a first home, but even then, the tax consequences can reduce the amount you actually receive. Another option some plans allow is a 401(k) loan, where you borrow from your own retirement account and pay yourself back with interest. While this avoids the penalty, it can still slow down the growth of your retirement nest egg.

For example, imagine someone withdraws $10,000 early from their retirement account. They could lose $1,000 immediately to the penalty, plus another chunk to income taxes. That $10,000 could have doubled or tripled in value by retirement, but instead, it shrinks drastically. That’s why financial experts strongly recommend leaving your savings untouched until you’re truly ready to retire.

👉 Next is H2: Rollover and Portability of Your 401(k) — do you want me to add a step-

Rollover and Portability of Your 401(k)

Changing jobs doesn’t mean leaving your retirement savings behind. One of the best features of a 401(k) plan is that it’s portable—you have several options for what to do with your money when you move to a new employer.

The most common choice is a rollover into an IRA or another employer’s 401(k). This lets your retirement account keep growing tax-deferred without triggering penalties or taxes. Rolling over also gives you more control, since IRAs usually offer a wider range of investment options than employer plans.

You could also choose to leave the money in your old employer’s plan, though that might limit flexibility. The least recommended option is cashing out, because you’ll pay taxes plus early withdrawal penalties if you’re under 59½. That decision can seriously reduce your retirement nest egg.

A simple way to think about rollovers is this: moving your 401(k) plan to an IRA is like transferring your money from one safe box to another, but keeping the lock intact. It protects your savings and ensures your long-term financial planning stays on track.

401(k) vs Other Retirement Accounts

While a 401(k) plan is one of the most popular retirement savings tools, it isn’t the only option available. Comparing it with other retirement accounts can help you decide which combination best fits your financial goals.

401(k) vs IRA

Both accounts offer tax advantages, but the main difference is contribution limits and investment choices. A 401(k) has higher contribution limits and often includes an employer match, while an IRA usually provides more investment flexibility.

401(k) vs Pension

A pension is funded and managed entirely by your employer, guaranteeing you a set income in retirement. A 401(k), on the other hand, depends on your contributions, employer match, and investment growth. Today, pensions are rare, making the 401(k) the primary option for many workers.

401(k) vs Brokerage Account

A brokerage account has no contribution limits and gives you complete control over investments. However, it doesn’t come with the same tax benefits as a 401(k). While a brokerage is great for general investing, a 401(k) is better for dedicated retirement savings.

Here’s a quick comparison for clarity:

| Feature | 401(k) Plan | IRA | Pension | Brokerage Account |

| Contribution Limits | High | Moderate | None (employer-funded) | None |

| Employer Match | Yes | No | Employer-funded | No |

| Tax Benefits | Strong | Strong | Guaranteed Income | None |

| Investment Options | Limited | Wide Range | Employer-controlled | Unlimited |

| Withdrawal Rules | Strict | Strict | Lifetime income | Flexible |

This comparison shows why most financial experts recommend starting with a 401(k) first, then supplementing with an IRA or brokerage account if you want extra savings and flexibility.

Common Mistakes to Avoid with Your 401(k)

Even though a 401(k) plan is a powerful retirement savings tool, many people lose out on growth because of avoidable mistakes. Here are some of the most common ones:

· Cashing out early

Taking money out before age 59½ often triggers a 10% penalty plus income taxes. This move shrinks your retirement account and steals away years of potential compound growth.

· Not contributing enough to get the employer match

If your employer offers matching contributions, not taking full advantage is like leaving free money on the table. Even small contributions can double thanks to the employer match.

· Ignoring contribution limits and catch-up opportunities

The IRS sets yearly contribution limits for a reason. Failing to max out contributions—or missing catch-up contributions after age 50—can slow down your long-term retirement savings.

· Overlooking fees

Some investment options inside a retirement account carry higher management fees. These may seem small, but over decades, they can eat into your returns.

· Sticking to one investment type

Putting all your money in stocks, or only in bonds, can backfire. A lack of diversification increases risk and may limit growth.

Avoiding these mistakes ensures your 401(k) plan works the way it’s designed—to build reliable, tax-advantaged retirement income for your future.

Smart Strategies to Maximize Your 401(k)

If you want your 401(k) plan to grow into a solid retirement nest egg, it’s not enough to just contribute. You need to be strategic. Here are some proven ways to maximize your retirement savings:

1. Contribute at least enough to get the full employer match

Think of the employer match as free money. Always contribute the minimum required to unlock the full match, because skipping it means losing out on guaranteed returns.

2. Increase contributions over time

Start small if you need to, but raise your contribution rate every year or whenever you get a raise. Even bumping it up by 1–2% can have a big long-term impact on your retirement account.

3. Take advantage of catch-up contributions after age 50

Once you hit 50, the IRS allows extra contributions beyond the standard limit. Using this feature helps you supercharge your savings in the years leading up to retirement.

4. Rebalance your investment mix regularly

Markets change, and so does your risk tolerance. Rebalancing your 401(k) investments ensures you stay diversified and aligned with your long-term goals.

5. Avoid high-fee investment options

Look closely at the expense ratios of funds in your retirement account. Lower-cost index funds often deliver better results over time compared to high-fee actively managed funds.

6. Don’t borrow from your 401(k) unless absolutely necessary

Loans from your 401(k) might seem tempting, but they reduce your growth potential. Plus, if you leave your job, you may have to repay quickly or face penalties.

By following these strategies, your 401(k) plan can grow steadily, giving you a more comfortable and financially secure retirement.

Conclusion

A 401(k) plan is one of the most powerful tools for building long-term financial security. It combines tax advantages, employer contributions, and a variety of investment options to help your money grow over time. By starting early, contributing consistently, and making smart investment choices, you can turn your retirement savings into a strong safety net.

Remember, the key to maximizing your 401(k plan is discipline and strategy. Whether you’re just beginning your career or nearing retirement, the steps you take today will directly shape your financial freedom tomorrow.

Your future self will thank you for making wise decisions today.

FAQs

1. What is the main benefit of a 401(k) plan?

The biggest advantage is tax savings and the opportunity for employer-matching contributions, which boosts your retirement savings.

2. How much should I contribute to my 401(k)?

Financial experts recommend at least 10–15% of your income, but at the very minimum, contribute enough to get the full employer match.

3. Can I lose money in a 401(k)?

Yes, since your money is invested in the market, it can fluctuate. However, long-term growth usually outweighs short-term losses if you stay invested.

4. What happens if I withdraw money early?

Early withdrawals before age 59½ typically come with taxes and a 10% penalty, which can eat into your savings.

5. What is a Roth 401(k)?

A Roth 401(k) is funded with after-tax dollars, meaning you don’t get an upfront tax break, but your withdrawals in retirement are tax-free.

Welcome To EarnproSavesmarter! I am realAnas an AI Powered SEO , Content Writer With 03 Years Of Experience.I Help Website Rank Higher, Grow Traffic ,And Look Amazing. My Goal is To Make SEO And Content Writing Simple And Effective For Everyone.

Let’s Achieve More Together.

Pingback: How to Make Money Online From Your Laptop in 2025